Divergent Stewardship in India: A Regulatory Blind Spot

Introduction

Proactive corporate governance and active stewardship are increasingly recognized as essential for safeguarding shareholder interests. With the objective of promoting a culture of proactive engagement, the Securities and Exchange Board of India (‘SEBI’) introduced the Stewardship Code (‘The Code’). The Code is a regulatory framework that guides an Asset Management Company (‘AMC’) in monitoring and influencing the governance practices of investee companies. Stewardship requires institutional investors to actively monitor their investments and engage with companies on matters such as performance and corporate governance. The purpose of such engagement is to create long term value for their clients. The Code’s primary objective is to ensure that institutional investor remain vigilant and intervene when necessary. This vigilance is intended to enhance market transparency and long term value creation. The Code was designed to ensure that AMCs take an active role in the governance of the companies in which they invest. In principle, such engagement should occur irrespective of the size of the holding. Even smaller stakes can be influential in promoting transparency and accountability. The Code’s framework builds upon existing principles implemented by SEBI regarding inter-alia voting for Mutual Funds. It requires institutional investors to formulate comprehensive and publicly disclosed policies on monitoring, intervention and voting. It also requires periodic reporting of these stewardship activities.

However, a critical examination of the Code reveals an important gap. The Code does not prescribe any threshold limit for triggering stewardship responsibilities. This silence has granted AMCs significant discretion in determining when stewardship activities apply. In practice, this ambiguity has led many AMCs to adopt self imposed quantitative thresholds in their internal policies. Based on an empirical analysis of the stewardship policies of 27 major AMCs in India (as of September 2025), this article identifies a concerning trend. Although the Code does not mandate any threshold, several AMCs require their shareholding to cross specified levels before actively engaging with investee companies. These thresholds are often 2%, 4% or 5% of total asset under management (‘AUM’) or paid-up capital. As a result, AMCs may monitor only those companies in which they hold a relatively large stake. Other companies may be ignored despite significant investments in them. Such companies may still warrant monitoring. However, they are left without meaningful oversight. This approach weakens the core objective of the Code.

The absence of regulatory direction has resulted in a wide divergence in stewardship practices. For instance, 360 ONE Mutual Fund applies a threshold of 2% overall AUM. Kotak Mahindra AMC employs a 2% holding requirement of net assets. Motilal Oswal AMC uses a threshold of more than 2% of the paid-up capital. In contrast, Franklin Templeton determines stewardship actions on a case-by-case basis. It takes into account factors such as materiality, the investee company’s track record and client interest.

This diversity of approaches highlights a significant regulatory gap. In the absence of a clear mandate from SEBI, AMCs are free to adopt practices that may narrow the scope of their stewardship activities. This narrowing may be intentional or unintentional.

Accordingly, this article proceeds in four parts. Part II sets out the methodology adopted for the research. It outlines the review of stewardship policies of 27 major AMCs in India. It also explains the criteria used to examine their threshold based engagement practices. Part III presents the empirical findings. It highlights the wide divergence in quantitative, qualitative and hybrid threshold approaches adopted by AMCs. Part IV then analyses how these varied practices expose regulatory gaps under the Code. The analysis focuses in particular on the dilution of active oversight, minority shareholder protection and regulatory arbitrage. Finally, the article proposes for regulatory clarifications.

Methodology

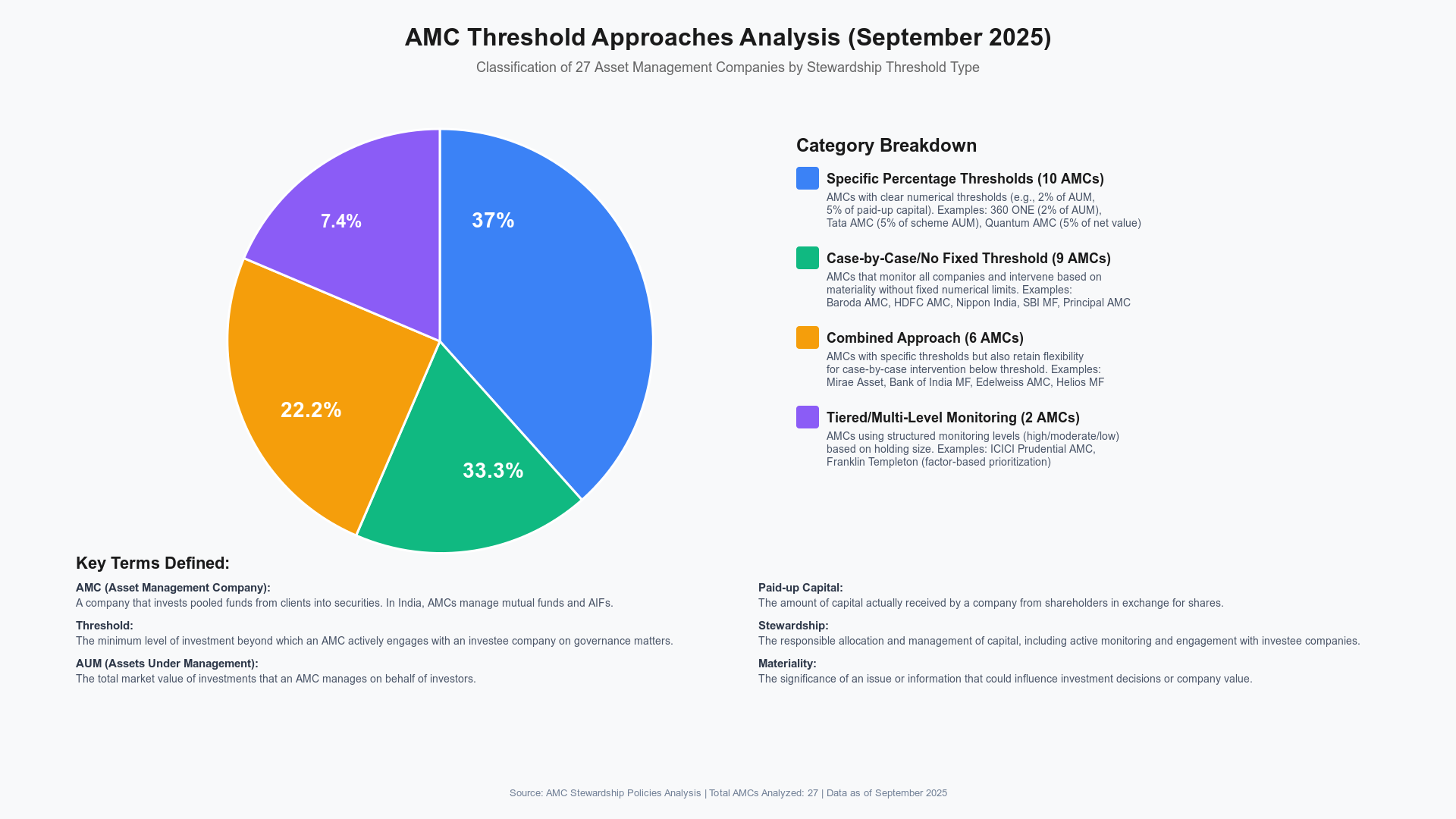

This study constitutes original empirical research and is based on an independent review of publicly available latest stewardship policy documents of 27 major AMCs in India as of September 2025. These AMCs were selected to capture a broad range of stewardship approaches including quantitative, qualitative and hybrid threshold models. This ensures a representative analysis of how stewardship responsibilities are implemented across the industry.

The policies referred to represent the latest versions disclosed by the respective AMCs on their official website as of the time of analysis. It is pertinent to note that the latest version of a stewardship policy may not necessarily bear a recent date (e.g., 2024 or 2025) as several AMCs continue to follow the versions introduced previously. Accordingly, references in this study are made to the most recent versions available irrespective of the year of issuance. The sample include institutions with diverse sizes, strategies, and market footprints. The primary focus is on the explicit threshold language used in their policies as documented in the AMC Threshold table.

The analysis centers on two dimensions. First, it examines quantitative thresholds where stewardship activities are triggered by specific numerical limits, such as a percentage of total AUM, paid-up capital or net assets. Second, it explores qualitative and discretionary criteria where thresholds are determined based on materiality or other case specific factors rather than fixed numerical values. Data was extracted directly from AMC website, annual reports and stewardship policy documents.

Refer to the AMC threshold table (hyperlinked).

Findings

The analysis reveals considerable variation in threshold practices among the sampled AMCs:

| I. Fixed percentage thresholds | · Helios Mutual Funds and LIC Asset Management both use a 5% threshold based on the paid-up capital of the investee companies as the trigger for active intervention.

· Kotak Mahindra AMC requires a 2% holding of net assets before engaging in stewardship activities, while Motilal Oswal AMC establishes a threshold of more than 2% of the paid-up share capital. |

| II. Case by case and materiality-based approaches | · Several AMCs, including Aditya Birla Sun Life AMC, and HDFC Asset Management, explicitly state that intervention decisions are based on a range of factors such as materiality, the criticality of the issue, and the size of the investment exposure.

· Meanwhile, ICICI Prudential AMC adopts a tiered monitoring approach (classifying its oversight into high, moderate, and lower levels) by considering both quantitative holdings and qualitative research inputs, which leaves room for significant discretionary judgment. |

| III. Hybrid models | · Bank of India MF employs a two-tier approach: advanced monitoring is triggered when the combined AUM exceeds 10%, while active participation is initiated only when holdings exceed 2% of an investee company’s paid-up capital.

· Meanwhile, Tata Asset Management Limited and Mirae Asset Global Investment apply fixed thresholds of 5% (of scheme AUM) and 4% (of paid-up capital), respectively, yet they retain the option to intervene below these thresholds on a case-by-case basis. |

| IV. Absence of inconsistency of thresholds | · Some institutions, such as HDFC Asset Management, Baroda Asset Management India Limited, and Principle Asset Management Pvt. Ltd., either monitor all investee companies or do not specify any threshold at all.

· In contrast, entities like ITI Asset Management mention only an impairment condition, a drop of more than 50% in fair value, without establishing a traditional threshold for monitoring. |

These findings show that even though the Code does not prescribe any threshold, many AMCs have adopted internal thresholds. Some thresholds are quantitative i.e. based on numerical cut-offs such as 2%, 4% or 5%. Others are qualitative i.e. based on non-numerical indicators such as materiality or criticality of the investment. These thresholds may limit the extent of active engagement by AMCs.

Bridging the Regulatory Gap

The empirical evidence raises several critical issues regarding the efficacy of the Code. First, the Code’s silence on the threshold limits creates regulatory ambiguity allowing AMCs to exercise considerable interpretative discretion. For instances, firms like LIC Asset Management and Helios MF set high thresholds around 5%, which effectively excludes many investee companies from active oversight. Discretionary approaches, like those used by Aditya Birla Sun Life AMC and Franklin Templeton, can be adjusted for each situation. However, the absence of standardized criteria leads to considerable differences across the industry.

Second, by imposing such thresholds, especially high ones, AMCs risk diluting active stewardship. If an AMC only intervenes when its holding exceeds 5% of an investee’s paid-up capital, significant exposures with lower percentages may go unnoticed and unmonitored reducing the effectiveness of the Code and weakening overall corporate governance. In addition to this, the basic principles of corporate governance instill that shareholders should exercise their voting rights. When minority shareholders fail to do so, it results in a concentration of power in the hands of the promoters placing minority shareholders at a disadvantage, therefore, undermining MF unitholders.

Finally, this regulatory ambiguity also opens the door to potential regulatory arbitrage. AMCs may adopt thresholds that allow them to bypass more onerous stewardship practices, effectively opting out of continuous monitoring and intervention to reduce administrative costs and compliance efforts. For instance, Tata Asset Management Limited (referred in the table above) has an AUM of Rs. 1.76 lakh crore (as of July 2024). Under its policy, enhanced monitoring and engagement are triggered only when an investment in particular company exceeds 5% of a scheme’s AUM. Even 5% of their total AUM amounts to approximately Rs. 8800 crore, which is an extremely large exposure by any standard. If a Tata Mutual Fund scheme invests, let’s say Rs. 8000 crore (around 4.5%) in Company X, it would still fall below the 5% threshold. As a result, despite having an investment worth thousands of crores riding on Company X, Tata Mutual Fund would not be obligated to conduct active monitoring or intervene even if the company shows signs of weak governance, mismanagement etc. This not only undermines the intent of the Code but also creates an uneven playing field where some AMCs engage more rigorously than others.

To address these concerns, the main task at hand is to standardise the triggers of stewardship responsibilites. This will ensure that the AMCs throughout the industry, regardless of their size, follow a consistent threshold. SEBI should clarify whether AMCs are permitted to impose internal threshold limits. It should either mandate a standardised threshold or eliminate such thresholds altogether. Where quantitative thresholds are considered necessary, SEBI should provide uniform benchmarks. For instance, a standardized approach, such as requiring active engagement for holding above a fixed percentage of AUM or paid-up capital, would reduce the scope for regulatory arbitrage and promote consistent stewardship practices across the industry. AMCs must also be required to disclose their specific thresholds and engagement criteria through regular, transparent reporting, enabling both regulators and investors to evaluate policy effectiveness.

The Indian and international approach to stewardship differs fundamentally. In India, compliance with the Code is mandatory, whereas internationally, stewardship codes function as a set of guiding principles based on a soft law approach, leaving their implementation to the discretion of institutional investors. This divergence can be attributed to SEBI’s retail investor first approach as the Indian market is dominated by a large base of small and relatively less informed investors who rely on institutional investors such as MFs, AMCs to act as responsible stewards of their capital. A mandatory framework ensure greater transparency, accountability and uniformity in stewardship practices strengthening investor protection. This underscores the need for SEBI to formulate and release a set of rules to ensure compliance with the Code and provide clarity.

Conclusion

The analysis of stewardship policies among 27 AMCs reveals a significant divergence between the intended spirit of the Code and the practices adopted by many institutions. The voluntary impositions of thresholds, ranging from as low as 2% to as high as 5% of key investment metrics, demonstrates how AMCs have used regulatory ambiguity to tailor their engagement strategies. While some firms employ case by case or materiality-based approaches, the overall effect is a dilution of active stewardship, potentially allowing governance issues in investee companies to go unaddressed. SEBI must provide explicit guidance on threshold limits to ensure the Code fulfills its mandate of promoting active investor participation and robust corporate governance. Clarifying or standardizing these criteria would not only close the existing regulatory loophole but also align Indian practices with global norms, thereby enhancing investor protection. In light of these findings, decisive regulatory intervention in required. By issuing clear directives SEBI can reinforce the fundamental purpose of the Code, ensuring that all investee companies are subject to vigilant and continuous oversight regardless of the holding size. Such reform is essential for fostering a more accountable and dynamic corporate governance environment in India.

*Siddharth Singh and Hemant Tewari are final year law students at the Dharmashastra National

Law University, Jabalpur.